TransUnion CIBIL, a leading credit information bureau, shared some insights on behavioural trends in consumer / business lending in India. TransUnion CIBIL now has records of 400mn customers, of which 185mn customers have access to live retail lending facility. Within this, 85mn customers fall in consumer lending segment and ~100mn in business lending and others (agri, PSL etc). The company adds 15mn -20mn through new to credit route, 15% of overall.

There is improving penetration (breadth rather than depth) is reflected in unique customer enquiry growth accelerating from 27% in Q2CY18 to 43% in Q4CY18. Encouragingly, single product single account customers constitute 40–45% (in terms of volumes) for Credit Cards, Personal Loans & Consumer Durable Loans. No doubt, the cross-selling trend is on the rise—multi product multi accounts (MPMA) up from 32% in FY16 to 37% in FY18. That said, asset quality behaviour is the best in this category given better seasoning.

Decreased Approval Rate

Now from supply perspective reflected in approval ratio, the rate has been consistently coming down by 10% points over last 2 years to 33%. This has started to reflect in moderating disbursement growth across all three buckets (consumer/business/others). Volume of data scrub seems high given robust traction in low ticket products but overall

disbursement growth is still modest.

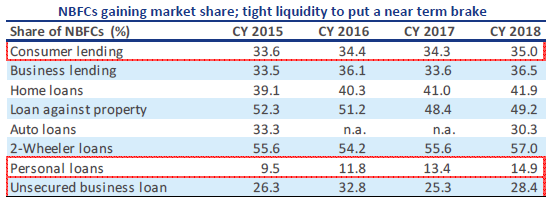

Rise of NBFC Lending in India

Looking at NBFCs, they have become significant player over past 3 years with market share rising to 35% in CY18 in consumer lending and to 36.5% in business lending. Further making segmentation, NBFC are seeing significant decline in real estate products. In contrast the NBFCs in consumer segment has seen significant buoyancy. In the near term, we expect tight liquidity to moderate growth at NBFCs in market share as well competitive product segments.

In the next article we will explore the Profile Distribution of Borrowers across various verticals of Bank / NBFC Financial Services.