We see an opportunity for Indian banks from the shift towards newer and inexpensive payment platforms and better penetration of non- balance sheet products like Credit Cards. Banks that make money through ATM interchange fees are likely to see higher income through debit / credit card transactions. On the other hand, a strong retail customer base, new products and focus can provide healthy wealth-management business.

We see an opportunity for Indian banks from the shift towards newer and inexpensive payment platforms and better penetration of non- balance sheet products like Credit Cards. Banks that make money through ATM interchange fees are likely to see higher income through debit / credit card transactions. On the other hand, a strong retail customer base, new products and focus can provide healthy wealth-management business.

Penetration levels have improved for debit cards (~40% of savings account customers) and a proper incentive structure should enable strong growth in fee income for all banks. We notice most of the fee income generated in the cards portfolio coming mainly through the ATM channel (infrastructure charges on ATM use by other banks’ customers) as debit cards primarily act as ATM cards for over 95% of customers.

Outstandings on credit cards are gradually increasing [Rs 25,000 Cr at End of Feb 2013] as banks are broadly comfortable with underlying origination checks (credit information bureaus and internal customers with a track record), current flow analysis (days past due across various buckets) and economic trends.

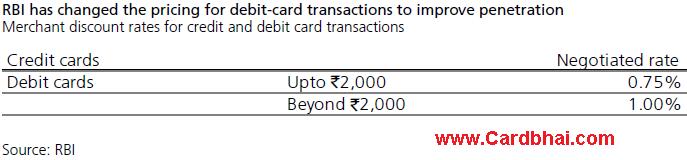

Most of the revenue from credit cards is from interchange fees, recovered through higher merchant discount rates (MDR). Debit cards do not include net interest income and are a much lower fee-income opportunity (mainly through regulated interchange income.

Fee income, after the recent change in guidelines, has a definite tilt towards the credit card business. In the next article we will see who are the leaders in the Indian Credit Card Business and how the Segment has grown in the last 5 years.